Knowledge sharing

Looking at issuer strategies: Wallets.

Digital wallets are the default way many consumers pay. The fight for banks to keep customers now happens on their phones, not in bank branches.

Digital wallets are the default way many consumers pay. The fight for banks to keep customers now happens on their phones, not in bank branches, because third-party digital wallets and apps (Apple Pay for example) offer a simpler daily experience that most users prefer.

Banks must figure out how to work with these same values, which are quickly becoming the standard for payments and even identity, or they will lose the customer relationship and simply become the invisible infrastructure running in the background.Issuers will need to think about their wallet strategy in order to:

➡️ Meet customer expectations for seamless, mobile-first payments.

➡️ Leverage tokenization for more secure transactions.

➡️ Drive engagement by being present in multiple digital ecosystems.Different wallet types highlight the complexity of choice:

➡️ OEM Wallets (Apple Pay, Google Wallet, Samsung Wallet): Core for NFC and in-app payments, often bundled with loyalty and ID verification.

Performance tracking, fraud analysis, and user adoption metrics are crucial to optimize value.

➡️ EUDI Wallets: Emerging in Europe, starting with digital identity but expected to store payment credentials. Integration choices (ID&V only vs. full payment) will be a key strategic decision.

➡️ Click to Pay: A scheme-managed cloud wallet (Visa, Mastercard, Amex, Discover) aimed at streamlining online checkout.

➡️ Merchant Wallets: Amazon, bol.com and others store credentials directly, driving recurring spend but fragmenting issuer visibility.

➡️ Third-party Wallets (PayPal, Alipay, WeChat Pay, Wero in Europe): Some start with P2P or online checkout and evolve into full multi-channel ecosystems.

➡️ Issuer NFC Wallets: Allow users to make NFC payments keeping the control within the Issuer’s mobile application.

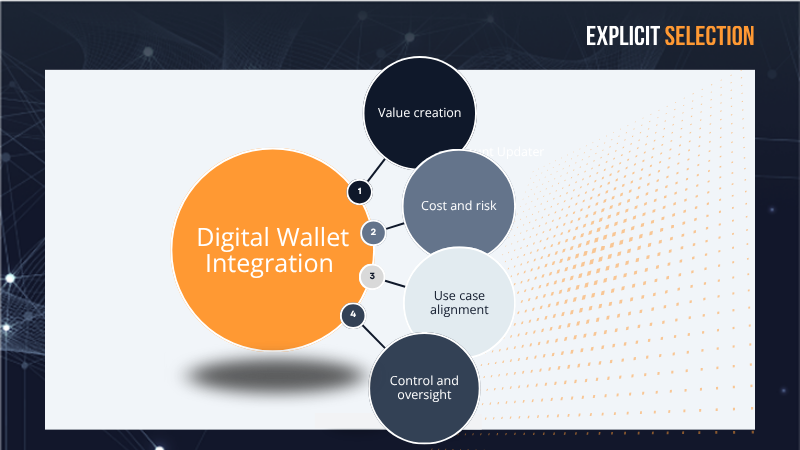

How Issuers can think about wallet integration:

𝐕𝐚𝐥𝐮𝐞 𝐜𝐫𝐞𝐚𝐭𝐢𝐨𝐧: Which wallets drive the most spending, engagement, or brand differentiation?

𝐂𝐨𝐬𝐭 𝐚𝐧𝐝 𝐫𝐢𝐬𝐤: Integration costs, contractual obligations, fraud exposure, and ongoing compliance need to be weighed carefully.

𝐔𝐬𝐞 𝐜𝐚𝐬𝐞 𝐚𝐥𝐢𝐠𝐧𝐦𝐞𝐧𝐭: Identity-first wallets vs. payment-first wallets serve different purposes, do you integrate with both, and how?

𝐂𝐨𝐧𝐭𝐫𝐨𝐥 𝐚𝐧𝐝 𝐨𝐯𝐞𝐫𝐬𝐢𝐠𝐡𝐭: Issuers (and end users) need a clear view of where credentials and tokens are stored, with tools to manage, suspend, or revoke them in case of fraud.

In conclusion, wallets have become a fragmented but critical battlefield for Issuers, requiring careful prioritization of integrations and ongoing control of credentials, and Explicit Selection can help banks cut through the noise, benchmark wallet options, and decide where to invest in.